One of the factors has made me want to post again is the repeated claims by the Realtors® and their shill MSM reporters that we’ve reached the “bottom.” If you look closely at the data, we’re still nowhere near the bottom.

I predicted years ago that the bottom would be reached by now. What I didn’t foresee was the massive amount of government intervention since the bubble burst. Back when I making predictions on the direction of the South Florida real estate market, I never expected TARP, all the various homeowners rescue bills, and the homebuyers’ tax credits.

I also didn’t expect the lenders to move so slowly on the foreclosure backlog. I have been hearing anecdotal stories of lenders not initiating foreclosure actions on borrowers that haven’t paid a cent on their mortgages for as long as two years. Of course, most of this is due to government intervention, somewhat through TARP, but mostly through rewriting the “Mark to Market” rules.

It’s these interventions in the market that has prevented us from seeing a bottom yet. But, it’s not like the public and its elected representative should have seen this coming – this is exactly what occurred in Japan a decade earlier in their bubble.

There’s an excellent article in Reason Magazine on this issue. Here’s a brief quote:

The scenario was eerily familiar. A long real estate bubble that had expanded extra rapidly for the previous five years suddenly burst, and asset prices came crashing back down to earth. Banks and financial institutions were left holding piles of worthless paper, and the economy soon headed south. The national government responded to the crisis by encouraging more lending and spending previously unfathomable amounts of money on public works projects in an effort to stimulate consumer spending and restart growth.

But that stimulus did not save the Japanese economy in the 1990s; far from it. The ensuing period came to be known as the Lost Decade, characterized by multiple recessions, an annual average growth rate of less than 1 percent, and a two-decade decline in stock prices and corporate profits.

The Japanese government’s easing of credit rates, instead of spurring real demand, created artificial demand. Federal loans and stimulus spending were not economically productive, and they vastly increased the nation’s debt and prolonged the economic malaise. Worse, businesses spent critical time on the sidelines, waiting for government bailouts and other centralized actions, instead of speedily consolidating their losses, clearing their balance sheets of bad investments, and reorganizing.

The United States in 2008–09, unfortunately, has started down the same path. Federal intervention and the expectation of additional government action are removing firms’ incentive to clean up their balance sheets by selling “toxic” assets. Why accept pennies on the dollar if a deep-pocketed new bidder (i.e., the state)

looms large on the scene? The Japanese experience shows that when the government is an active participant in the market, many firms would rather accept state support than initiate the inevitable financial reckoning. Such a status quo does

not provide a sustainable foundation for the economy. Instead, it restricts

economic growth and creates a cycle of stagnation.

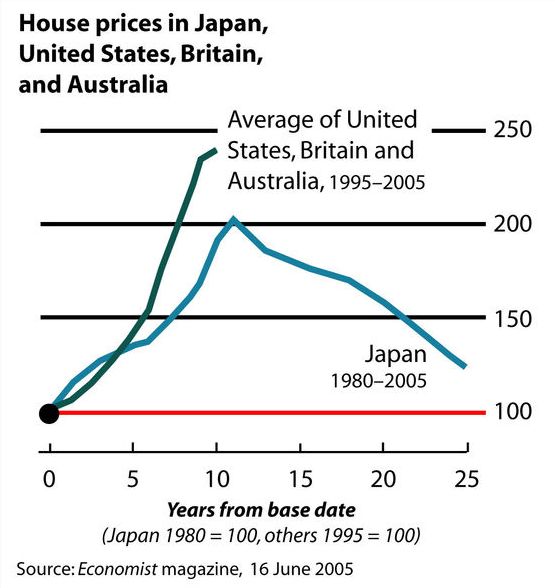

And when we look at a graph of Japanese housing prices compared to ours, we can see we may have a long way to go:

After its crash, Japan took 15 years to reach its bottom. Unfortuantely, we're only 4 to 5 years into our real estate crash. We may have a decade to go.

Stumble It!

Stumble It!